High level decisions

When it comes to getting your next car, there are a number of alternatives, which are explained in more detail below.

There are many different ways to run or buy a vehicle; Cash, Loan, Hire Purchase, Personal Contract Hire, Personal Contract Plan.

Some people love to drive a brand new car or prefer nobody else to have driven it but remember the car will depreciate quickly and you are paying brand new car tax as well.

Depreciation is the difference between a car's value when you buy it and when you come to sell it. This drop varies between makes and models but typically is between 15-35% in the first year and up to 50% or more over three years.

Some people will wait 3 years until the 50% depreciation has come out and then buy. But vehicles will continue to depreciate up to 10 to 12 years before the vehicle stops losing money.

Buying a car

If you buy a car. you do own it, but we advise you to do the numbers. Today many thousands of drivers are opting for leasing or PCH or PCP. Whereby you can lease a vehicle each month and at the end of a given time hand the vehicle back and get a new one and start all over again. There are lots of benefits and peace of mind about leasing a car.

You can take a loan or Hire Purchase and pay for your car that way but again remember the longer the loan term and the depreciation on the car could leave you losing out.

Often Leasing, PCP, PCH are not good if you’re doing high mileage and there are penalties for going over the prescribed mileage.

Pay cash

This way the car is yours immediately. You will spend less time in the dealership buying it, although it may not be the best deal (if the dealer offers cheap finance) or special offers.It's great if you can afford it. You're free of monthly repayments and interest. You can also often negotiate a discount, especially when buying privately.

There's a strong argument NEVER to mention that you're paying cash if you're buying from a car dealer. That's because dealers only make 28% of their profits from the car: the rest is from warranties, service. extras, etc. See the video - it's a US video but the logic is the same. It explains how you negotiate with a dealer if you pay cash.

Be sure to research prices if you're buying a new or used car using WhatCar or Parkers.

Taking out a loan to buy the car

If you want to borrow money to buy a car, your bank or building society is likely to be cheaper. You should make sure you can afford the repayments (see BudgetDrive) and you get the best rates.

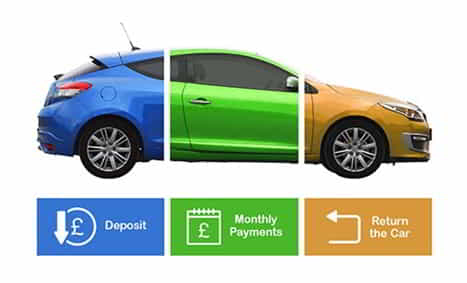

Personal Contract Hire PCH

If you’re looking to hire a car long term and don’t want to buy it, the cheapest option is likely to be using PCH.

What is personal contract hire PCH?.

According to Arnold Clark "Personal Contract Hire (PCH) is the long-term lease of a brand-new vehicle. PCH is different to Personal Contract Purchase (PCP) as a PCH vehicle cannot be purchased at the end of a lease, unlike PCP vehicles. During the lease agreement, fixed monthly payments of a PCH vehicle will be discussed, as well as an agreed mileage and time period for the lease."

Personal Contract Plan PCP

PCP is similar in many ways, but lets you purchase the car at the end of the agreement.

It's a way of financing new or used cars. It effectively works as a long-term rental, meaning you'll be able to drive the car until the contract ends. PCP deals have become a popular type of car finance as they typically offer lower monthly payments, making newer and expensive cars feel more affordable.

Traditional Hire Purchase?

For many years people who could not afford to buy the car outright would take out a car loan or hire purchase agreement.

Hire purchase (HP finance) is a way to finance the purchase of a new or used car. Usually, you put down a deposit and then pay the cost of the vehicle in monthly instalments, with the finance secured by the car's collateral. This means you do not own the car until the last payment is made.

You can get a quote from CarPlus

Insuring your car

The first thing is getting you the best deal to meet your needs and that is important; it is also worth considering maintaining the search for future by having specialists search for the best suitable product every year.

You can see more about car insurance and other forms of insurance in InsuranceDrive

Selling your car

There are many options for selling your car. You need to decide on how is best for you.

In summary some options include:

Sell privately

You’ll probably get a better price selling a car privately, but it can be time-consuming and there are some pitfalls, Here are some thought

You’ll need to:

Sell privately online

These days there are an enormous number of choices for selling your car online.

You can place an online ad in Auto Trader (which costs you money - £36.95 to £74.95, so make sure you read the guidelines) and as they have 7 million web visits a month it should sell. It connects buyers and sellers, so see previous section!

There are other sites but they don't have the same traffic - look at Motors.co.uk

You can also use eBay and Gumtree. These days eBay allows you to create a resrve price and auction your car off to the highest bidder, and there are other online auctions, including salvage cars and seized vehicles .

Instant Cash Offer

You will have seen or heard these sites advertised - basically you enter your registration number and get an offer. The car has to be inspected and then the offer is finalised.

Sometimes the company do it themselves - webuyanycar has a network where you take your car to be assessed.

Motorway value your car immediately then get the highest price from dealers; your car is picked up from home and the service is 'free' as the dealers pay! Carwow is similar and Motorway value your car immediately then get the highest price from dealers; your car is picked up from home and the service is 'free' as the dealers pay! Cazoo are more like webuyany car.

Sell at auction

You normally pay an entry fee (c. £30). You set a reserve price, take it to the auction and then they try and sell it.

If someone buys it, they pas for it immediately and the auction company gives you the sale price less its commission, which can be up to 10% of the sale price.

Bigger car auction companies such as British Car Auctions have branches throughout the country, but there are independent auctioneer which may be more local.

There are some things you MUST be aware of before going to an auction (especially for the first time. Look at 12 essential tips on Hagerty - a US site which makes some good points.

Selling to a dealer

One of the most popular ways of selling your car to a dealer is to part exchange when you trade in your old car for a new one.

This essentially involves two deals being done in one transaction. Normally, you’ll trade in your old vehicle, for a newer, more expensive one. You then pay the difference – either by paying the extra money to the dealership or by taking out finance on the new car. This might be easy but it isn't always the most cost-effective way of doing things - dealers will make money on both transactions and it may be better to sell outright first then buy.

You can sell your car to a dealer without buying another car; some dealers prefer certain makes. You will also have to negotiate!