Creating and managing a budget isn’t easy - it’s an art

Learning to budget is not just about saving on the weekly shop but your whole finances

Forming a budget is the first step when building a solid financial foundation. The goals of a personal budget are as follows:

- Quickly show your “before expenses” and “after expenses” estimated balance

- Track paid vs pending expenses

- Track upcoming expenses (forecasting)

- Track the amount of money going to each expense

- Identify and develop trends to optimize your budget

Keeping the budget simple and building upon it is a great way to get started.

More than 1 in 5 (22.9%) say they make impulsive purchases every week

How to stop impulse buying

Avoid temptation. The best way to stop an impulse purchase? ...

Stop and consider. ...

Create and stick to a budget. ...

Think about your motivations to make an impulse purchase. ...

Limit your cash and credit. ...

Stay off social media. ...

Remind yourself of your goals.

Map out your financial plan

We have done our own 10 step financial planning template you can look at and download. It doesn’t just consider how to do a budget, but gives some tips on how to decide what’s important to you and how to balance the short term immediate issues with looking to the future.

Following this will give you ideas on how to prioritise your spending.

It's not trite stuff about spreadsheets - it considers what's most important to you. We guarantee that following these 10 steps is a realistic way to approach your budgeting and financial life.

See the plan below, with the 10 steps set out under five headings.

Tips for doing your budget

There are loads of tips online for doing your family budget – we’ve come up with our favourites in this list:.

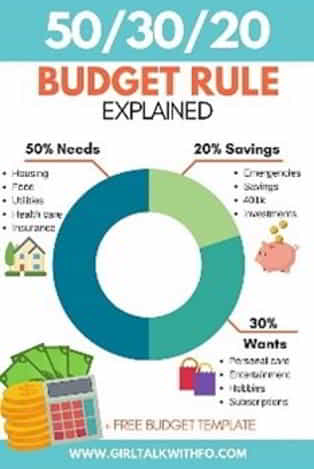

We can recommend the 50/30/20 rule, which breaks down your after-tax monthly income into three budget categories:

1. Needs

These are expenses that you must pay in order to live and work, such as a mortgage or rent and groceries. They should account for about 50% of your spending.

2. Wants

These are expenses that don’t qualify as needs and don’t include your savings and payments toward debt. If you can live and make money without it, it’s probably a want. This should be 30% of your spending. Wants vary widely according to who you are and your situation, so someone's needs are someone else's wants. .For example, if you go to the gym as part of your training for your career as an athlete the costs are needs, but if it's to keep trim it’s a want.

3. Savings and debt repayment

This category includes expenses that help your future self and should account for 20% of your income. Use this category for building an emergency fund and setting aside money for retirement.As for debts, focus first on high priority debt you may have, such as high-interest credit card or other loans (see DebtDrive). This category could also include payments beyond the minimum balances on lower-rate debts, like a mortgage. (See DebtDrive to see the difference between good and bad debt.)

What are the main reasons we impulse buy?

Enjoyment, we tend to pick up things that make us happy.

Loss aversion.

Spending on children who you feel may deserve a treat.

Short term injection of pleasure when feeling depressed.

Thinking you've spotted a bargain.

The need to stockpile.

Simple tips help you avoid impulse buying instore and online

Time Out! Come across something that you would like to buy?

Shop with a list

Don't buy for the wrong reasons.

Use cash instead of credit card.

Give yourself a no-spending challenge

Don’t Shop when hungry or drunk

Spend within budget.

Avoid online spending whilst intoxicated, you will always regret it.

Unsubscribe from retail newsletters, mailers and special deals

Think about the last purchase you regret

Become a switcherholic

Less than 50% of people change house, car, contents, credit cards, mobile and internet contracts every year. Most people do not get into the habit of switching their may suppliers every year. Statistically people switch every 3 to 4 years because they cannot be bothered..

One of the main reasons for not switching is because it is seen as a chore with 43 per cent of over 24-year-olds saying it is a hassle – a figure which rises to 55 per cent amongst 18 to 24-year-olds. This is money.com